The accompanying analysis and charts explain how each story is creating ripples on the global stage, where it is headed in the coming weeks, and whether it can have an impact on India.

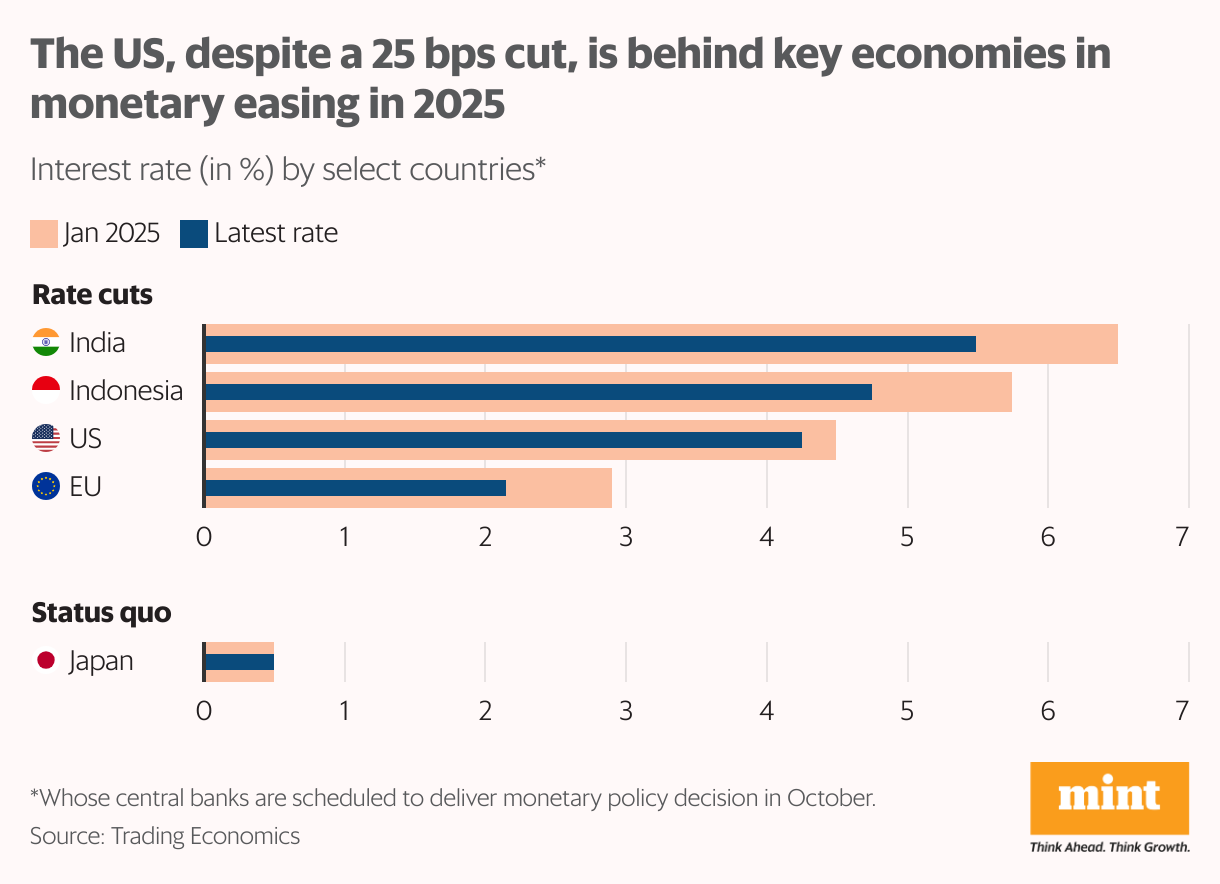

Policy at ease

The US Federal Reserve finally joined major central banks in easing monetary policy by 25 basis points (bps) last month, delivering its first rate cut since December. Since other major central banks had already begun the easing process, the Fed’s cuts are likely to continue in the coming months, with an indication of at least another 50-basis-point reduction.

This will keep all eyes on the upcoming meeting at the end of October. The central banks of India, Indonesia, and the European Union are also scheduled to deliver their monetary policy decisions.

Views are divided on whether India will go for another rate cut after having delivered 100 bps of cuts since February amid strong 7.8% GDP growth in April-June. The Reserve Bank of India’s Monetary Policy Committee is scheduled to announce its decision on 1 October.

Similarly, Indonesia and the EU have also eased their monetary policies, and the Fed’s latest cut is unlikely to weigh on their decisions.

The Bank of Japan, however, may move in a different direction, with a rate hike soon, continuing its policy of moving away from ultra-accommodative policy due to signs of durable inflation and wage pressures.

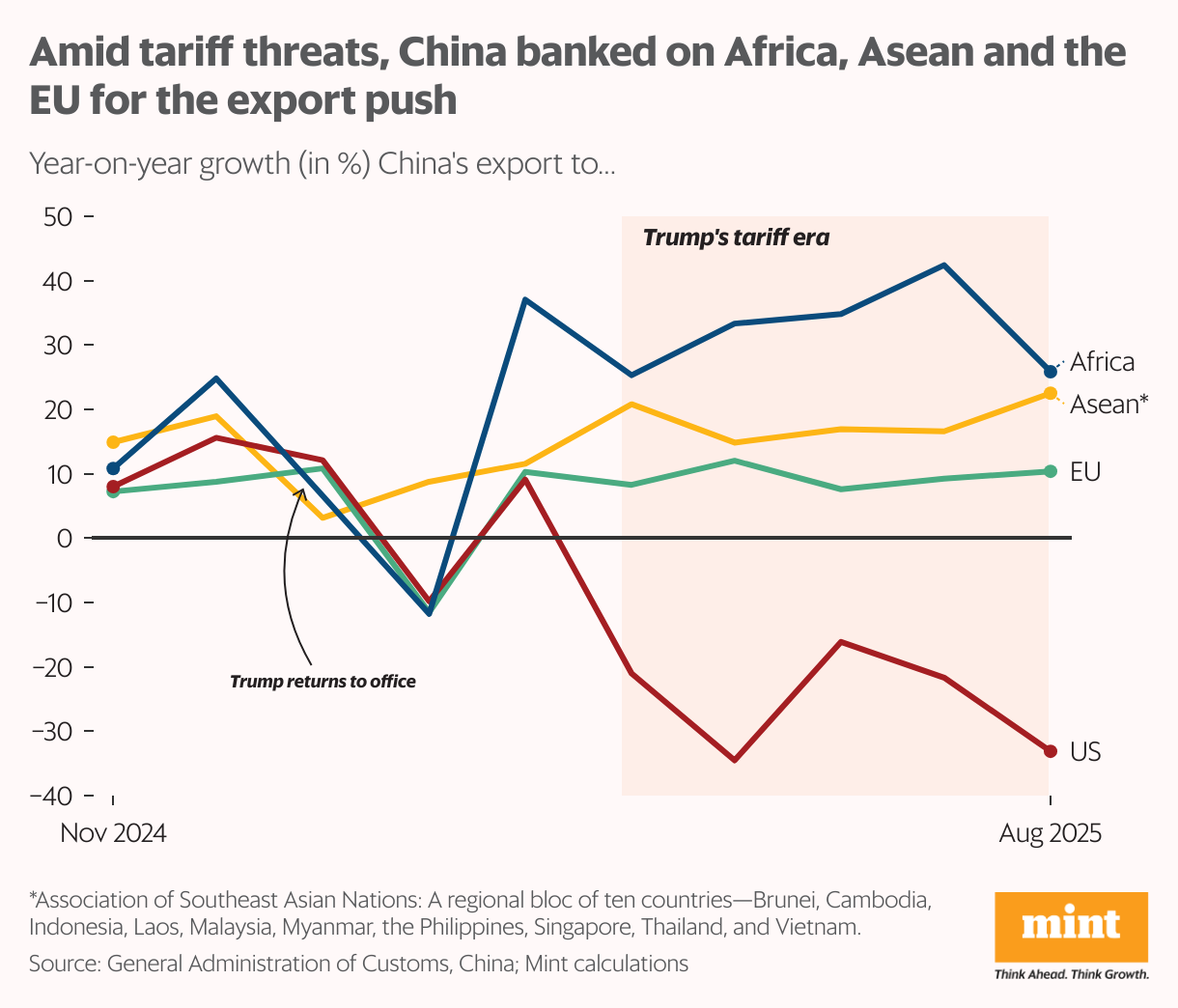

Dragon’s destinations

As the US’s tariff threats loomed, China was quick to calibrate its export policy, shifting the shipment of goods more towards Africa and Asean nations.

The year-on-year decline in China’s exports to the US, which began in April, was exacerbated in August (-33%) after the 90-day pause in the US’s reciprocal tariffs ended. This took a toll on China’s overall exports, which grew 4.4%—the slowest pace since February. However, at the same time, export growth to Africa, Asean nations, and the EU was 25.8%, 22.5% and 10.4%, respectively, in August.

When Donald Trump was elected the US president in November, Africa, Asean, and the EU, along with Washington, had similar export growth levels. Their paths began to diverge as months went by, and Washington’s protectionist policies became clearer.

Since China is currently facing over-capacity and low producer prices, experts believe some of the export growth is part of its re-routing strategy to circumvent high tariffs. Most Asean nations are facing 19-20% tariffs, while the effective tariffs on China can be upwards of 30%.

Border barriers

Since returning to office in January, Trump has tightened US immigration policies to unprecedented levels in some contexts, widening the net to cover even legal immigrants.

The White House has rolled out measures making it harder for international students, skilled workers, and even legal residents to stay in the country.

Visa programs have been hit with steep fees, including a $100,000 application charge for new H-1B visa applications, while vetting has expanded to include applicants’ social media and political views.

Refugee admissions have been largely frozen, and citizenship tests have been toughened, with the administration reviving “neighbourhood checks” and rescinding Biden-era guardrails on denaturalization investigations.

The State Department has already revoked more than 6,000 student visas this year, nearly four times last year’s level.

Together, the measures mark one of the most aggressive clampdowns on legal immigration in decades, reshaping how people can study, work, or settle in the US. The steep one-time H-1B visa fee for new applicants will particularly hit Indians, as they make up over 70% of the total approvals.

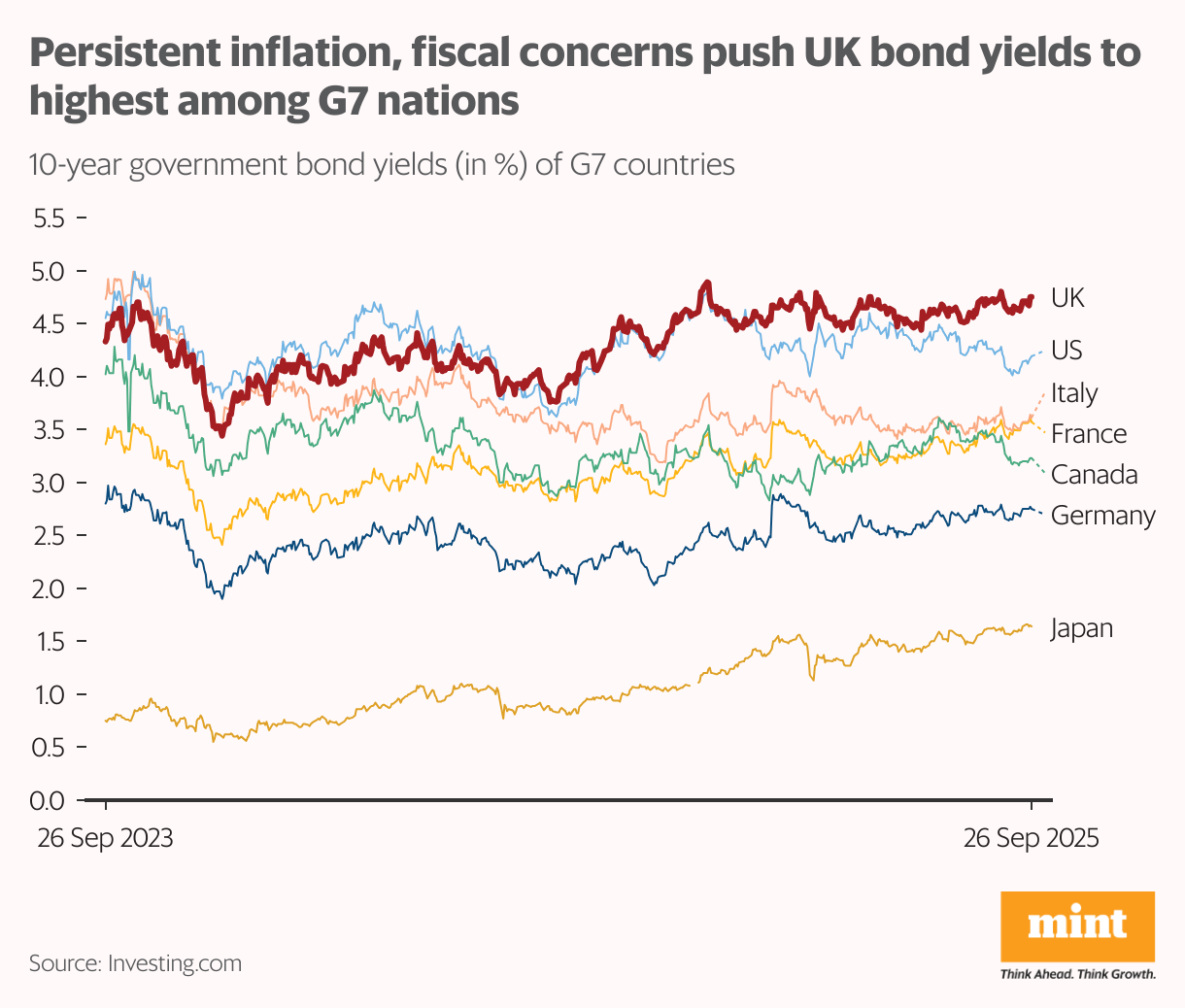

Yield watch

The UK’s 10-year government bond yields have climbed to around 4.8%—the highest among the G7 economies—due to persistent inflation, tight monetary policy and unusual supply pressures in the gilt market in the country. This signals that investors are seeking more returns for lending money to the government due to concerns over fiscal credibility—the UK’s debt-to-GDP ratio is close to 100%.

Moreover, with consumer prices still running well above the euro-zone average, the Bank of England has held interest rates at 4%, which is about twice the level of the European Central Bank’s.

On top of this, the UK government is actively engaging in quantitative tightening, selling government bonds it previously bought during the covid-era quantitative easing.

While yields of other G7 nations are not as high as those of the UK, they too have displayed a rising trend over high debt levels in these countries.

The situation is precarious, as the pessimism seen in the UK could spread to other markets and trigger risks for the rest of the world.

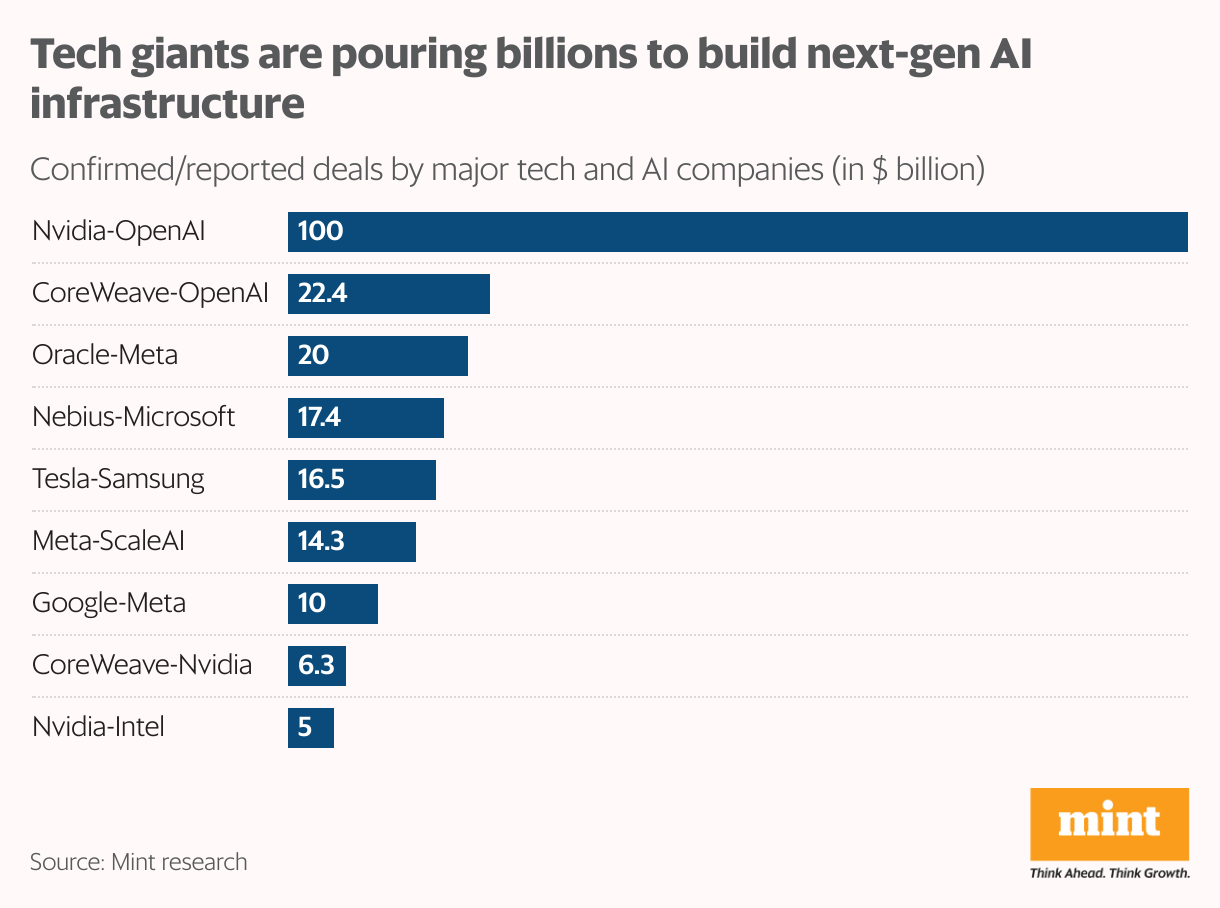

Eye on AI

Global tech giants are accelerating investments in artificial intelligence as demand for generative AI has surged across industries.

Nvidia Corp. is leading the charge with a $100 billion investment in OpenAI for supplying data center chips, giving the chipmaker both a financial stake and strategic influence in one of the world’s top AI firms. According to a Reuters report, this is part of a broader wave of multi-billion-dollar deals reshaping the AI landscape. Cloud and infrastructure partnerships are central to this push.

Oracle Corp. is expected to provide OpenAI with $300 billion in computing power over five years, while Meta Platforms Inc. and Google (Alphabet Inc.) have signed cloud deals exceeding $10 billion.

Hardware providers are not far behind: Intel Corp. received $2 billion from SoftBank Group, CoreWeave signed multi-billion-dollar contracts with Nvidia and OpenAI, and Tesla Inc. is sourcing AI chips from Samsung Electronics Co. Ltd for its next-generation vehicles.

While AI is becoming a core business strategy, particularly among tech companies, it has also led to worries over job cuts. According to layoffs.fyi, more than 200 companies across the world have cut over 90,000 jobs in 2025 so far, with many of them linked to a transition towards greater usage and integration of AI.