Every month, Mint’s Plain Facts gives you an update on key global data to help you thread together the biggest developments worth paying attention to.

The accompanying analysis and charts explain how each story is creating ripples on the global stage, where it is headed in the coming weeks, and whether it could have an impact on India.

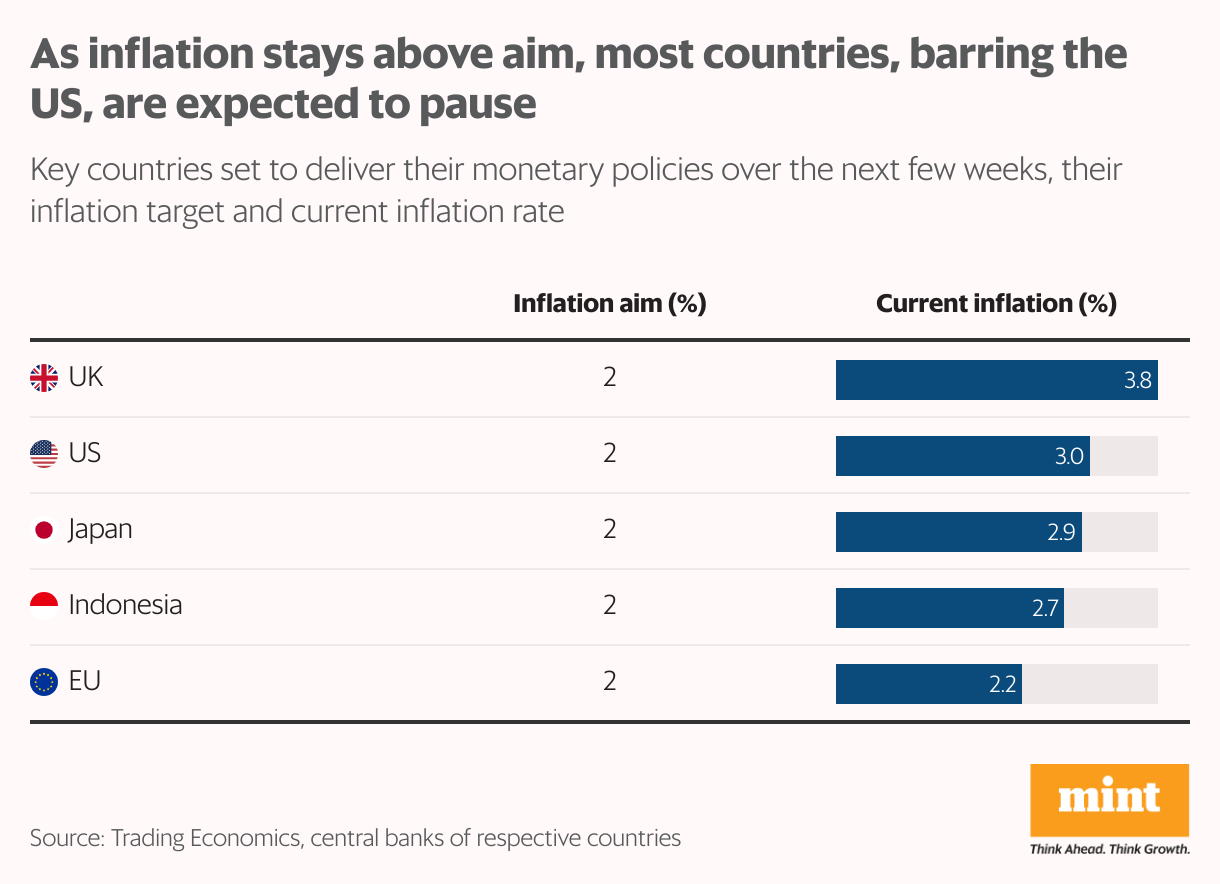

To cut, or not to cut

Global uncertainty and trade tensions demand easier credit flow to keep growth momentum intact. This year, several countries and blocs eased their monetary policies to support growth, and the US Federal Reserve joined them in September. As inflation remained high in many advanced economies, the policy moves were difficult to take, resulting in non-synchronised rate cuts over the months. The monetary policies of the US, UK, Japan, Indonesia, and the European Union (EU) are expected to remain on different tracks.

The Fed, scheduled to announce policy on Wednesday, is widely expected to cut rates by another 25 basis points even though inflation is 100 basis points above its target, owing to weak a job market. On the other hand, the Bank of England (BoE) and the European Central Bank (ECB), which have already cut rates by 75 basis points and 100 basis points, respectively, are expected to pause and remain data-dependent. The Bank of Japan (BoJ), which is focused on achieving its 2% inflation target, is expected to remain on pause.

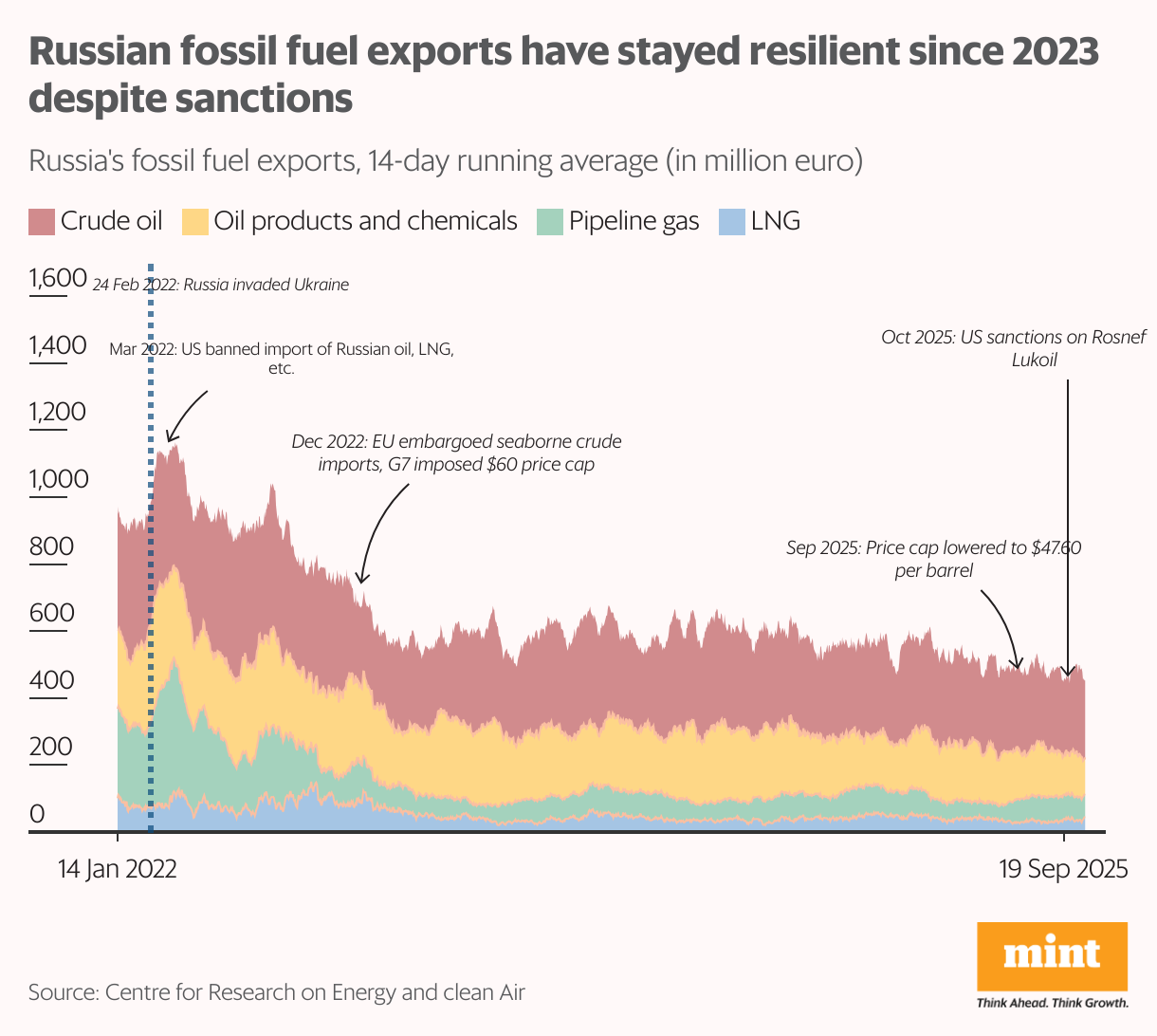

Slippery sanctions

Since the start of the war in Ukraine, the US, EU and their allies have imposed all types of sanctions on Russia. The latest sanctions from the US target Russia’s largest oil firms, Rosneft and Lukoil, aiming to cut Russia’s revenue streams from fossil fuels, which have not seen a significant dip despite several rounds of sanctions over the years. Russian exports of key fossil fuels, including crude oil and piped gas, had a 14-day running average of €1 billion, which dropped to around €600 million by 2023 but have remained around €400-500 million since then.

There are several reasons why sanctions have so far proved inadequate in dismantling Russia’s war machine. For one, China and India continue to buy large quantities of Russian oil. Second, many European countries have drastically reduced the use of Russian oil and gas but haven’t been able to cut it out entirely because of a lack of suitable alternatives. Third, Russia has managed to find way to evade sanctions, reportedly by using intermediaries, alternative payment systems, and shadow fleets.

China’s growth gap

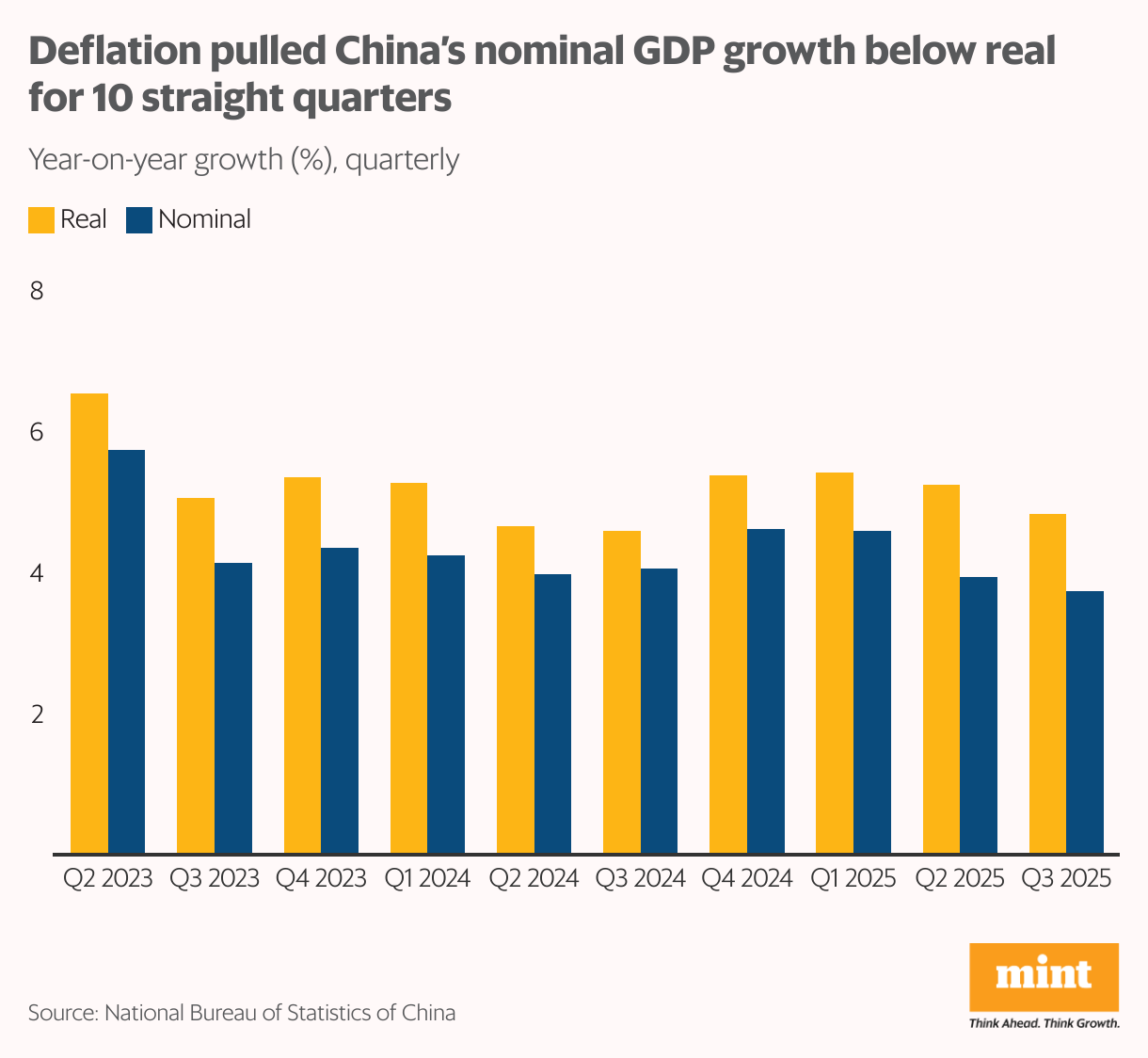

China’s GDP growth declined to 4.8% in July-September, below the 5% target for the first time in four quarters, owing to trade tensions with the US and continuing problems in the property market. While real growth is still close to the goal, nominal growth paints a picture of slow growth momentum. China has faced deflation for several months now, reflecting weak consumer demand and industrial overcapacity, resulting in low growth at current prices. Nominal growth has been 50-130 basis points lower than the real growth rate in the past 10 quarters.

Prices are falling in China does not bode well for investment intentions and wage growth, both of which are currently being overshadowed by the fiscal stimulus the Chinese government announced last year. Slowing growth in China is a concern for the world because of the country’s deep links in trade and investment. Deflation is particularly worrying as it allows China to dump cheaper goods into other markets, potentially hurting competitiveness.