Markets opened the week in a risk-on mood as trade developments filled the void left by a barren economic calendar. Euro gained broadly following the announcement of the US–EU framework agreement over the weekend, although upside momentum remained modest. The deal eased tariff threats and highlighted strategic cooperation, including major European energy purchases from the US.

Aussie and Kiwi also posted gains, supported by improving sentiment. In contrast, Dollar, Yen, and Swiss Franc were weaker across the board—a clear sign of waning demand for defensive assets. Loonie and Sterling were little changed, trading in the middle.

The broader market awaits a heavy slate of events later in the week, including monetary policy decisions from Fed, BoC, and BoJ. On the data front, traders will monitor GDP and inflation figures out of the US, Eurozone, Australia, and China for macro signals heading into August.

Nevertheless, immediate focus will shift to Stockholm first, where US and Chinese negotiators meet today into determine whether their fragile tariff truce can be extended beyond the looming August 12 deadline. Treasury Secretary Scott Bessent and Vice Premier He Lifeng lead the talks, which could set the tone for a possible Trump–Xi summit later this year.

Bessent has already suggested that the US is willing to delay tariff reimposition if talks progress. However, Beijing is expected to press for deeper cuts to the layered US tariffs, now totaling 55% on most Chinese goods, and for relaxation of technology export restrictions.

Parallel to the Stockholm dialogue, South Korea is reported to be pursuing an ambitious “Make American Shipbuilding Great Again” proposal to avoid the 25% US tariff. Officials from Seoul are in talks with the US this week, seeking to finalize a deal before Trump’s August 1 deadline. A cooperative framework on shipbuilding is being discussed as the centerpiece.

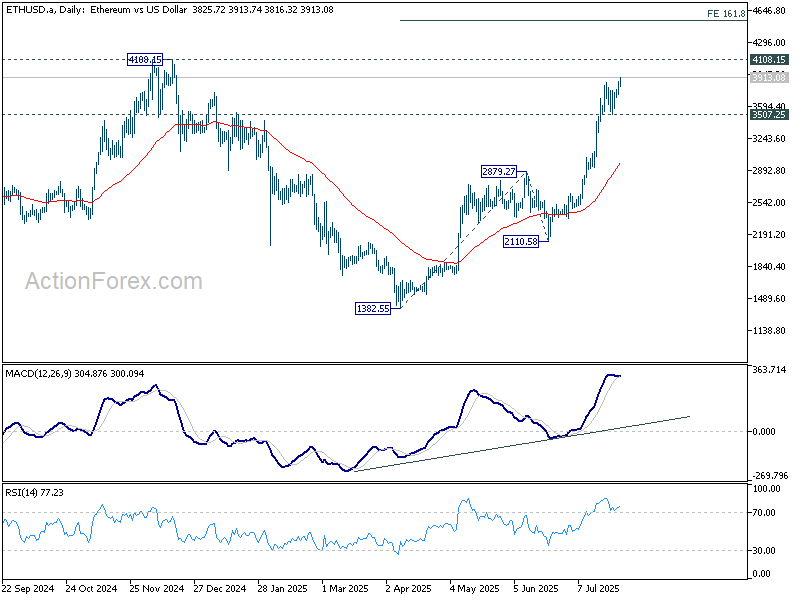

Technically, Ethereum’s up trend resumed today and breaks above 3900 mark. Near term outlook will now stay bullish as long as 3507.25 support holds. Next target is 4108.15 high. Firm break there will target 161.8% projection of 1382.55 to 28179.27 from 2110.58 at 4532.27.

In Asia, at the time of writing, Nikkei is down -1.06%. Hong Kong HSI is up 0.53%. China Shanghai SSE is flat. Singapore Strait Times is down -0.24%. Japan 10-year JGB yield is down -0.04 at 1.565.

US-EU trade deal delivers Relief, Euro gains but lacks breakout momentum

In a significant breakthrough, the US and EU reached a framework trade agreement on Sunday, averting the imposition of 30% tariffs on European imports. Instead, a reduced 15% rate will apply to most goods. The two sides also agreed to exempt key strategic sectors—such as aircraft, chemicals, and some pharmaceuticals—from any tariffs entirely.

The deal also includes sweeping commitments from the EU, including USD 750B in US energy purchases and USD 600 billion in fresh US-bound investment over current levels.

EU Commission President Ursula von der Leyen called the agreement a win for “stability and predictability,” while acknowledging that the 15% tariff still presents challenges for European automakers. Meanwhile, the EU’s pivot toward US nuclear fuel and LNG also marks a decisive shift away from Russian energy dependency.

US President Donald Trump declared the deal as larger than last week’s USD 550B Japan agreement and reiterated that it would significantly deepen US-EU ties across energy, defense, and trade. He claimed “hundreds of billions” in arms sales could follow.

Euro advanced broadly on the announcement, but momentum is restrained. EUR/CHF is still capped below 0.9365 resistance despite today’s bounce. Firm break of this level is needed to be the first sign that consolidation pattern from 0.9445 has completed, and the rally from 0.9218 is ready to resume. Otherwise, more sideway trading would likely follow first.

Fed, BoC and BoJ to hold, as data wave hits global markets

A busy week lies ahead, packed with three central bank decisions and critical macro data. Fed, BoC and BoJ are all due to announce policy decisions, while top-tier reports on growth and inflation from the US, Eurozone, Australia, and China will shape investor expectations heading into August.

Fed is widely expected to leave interest rates unchanged at 4.25–4.50%. The key intrigue lies in whether dovish-leaning governors Christopher Waller and Michelle Bowman will formalize their views by voting for a cut, and if others on the FOMC might join them.

Futures markets are pricing in around a 65% chance of a September cut. However, Chair Powell is unlikely to pre-commit or even give any concrete guidance. Instead, traders’ focus will turn to Q2 GDP advance and June PCE inflation report. July’s non-farm payrolls and ISM manufacturing data will soon follow, giving markets ample fodder to reassess the Fed outlook.

BoC is similarly expected to hold rates at 2.75%, pausing for a third time in this cycle. Earlier fears of deep recession from US tariff escalation have eased, as CUSMA exemptions ensure most Canadian exports remain duty-free.

On the other hand, Canadian inflation has surprised to the upside, challenging assumptions that weak demand would lead to faster disinflation. The BoC’s cautious stance reflects the need to see clearer signs of core inflation cooling before taking further steps.

Market consensus still leans dovish. A Reuters poll found that nearly two-thirds of economists expect a BoC cut in September, with most seeing at least two total reductions in 2025.

BoJ is also set to hold steady at 0.50%, but its outlook is evolving. Deputy Governor Uchida sounded notably upbeat last week, pointing to diminished uncertainty and stronger prospects for achieving sustained 2% inflation following the US–Japan trade pact.

BoJ will factor the trade deal into its quarterly projections this week, potentially teeing up policy tightening later in the year.

Beyond central banks, attention will also turn to Eurozone GDP and CPI, Australia’s CPI and retail sales, and China’s PMIs for additional global growth signals.

Here are some highlights for the week:

- Tuesday: US goods trade balance, house price index, consumer confidence.

- Wednesday: New Zealand ANZ business confidence; Australia CPI; Eurozone GDP; Swiss KOF; US ADP employment, GDP advance, FOMC rate decision; BoC rate decision.

- Thursday: Japan industrial production, retail sales, BoJ rate decision; Australia retail sales; China NBS PMIs; Germany CPI flash, unemployment; Eurozone unemployment rate; Canada GDP; US personal income and spending, PCE inflation, Chicago PMI.

- Friday: Japan unemployment rate, PMI manufacturing final; Australia PPI; China Caixin PMI manufacturing; Eurozone PMI manufacturing final, CPI flash; UK PMI manufacturing final; US non-farm payrolls, ISM manufacturing.

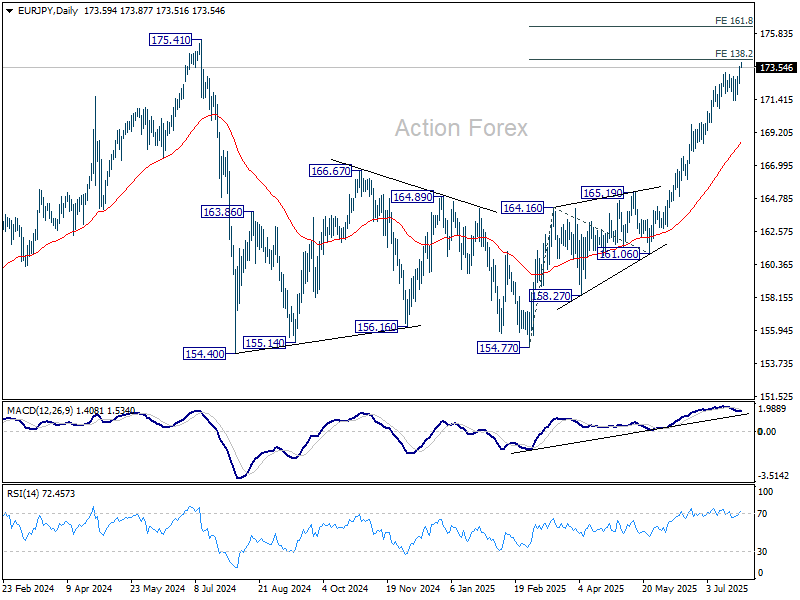

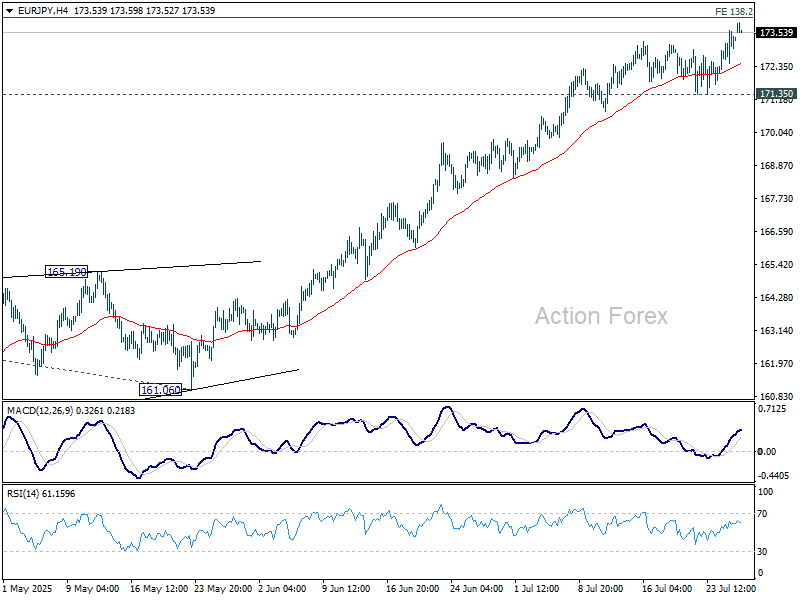

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.67; (P) 173.14; (R1) 173.81; More…

EUR/JPY’s rally continues today and intraday bias remains on the upside. Immediate focus is on 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03. Break there will bring retest of 175.41 high. For now, near term outlook will remain bullish as long as 171.35 support holds, in case of retreat.

In the bigger picture, considering current strong momentum as seen in the rally from 154.77, corrective pattern from 175.41 could have already completed. Decisive break there will confirm long term up trend resumption. Next target is 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, rejection by 175.41, followed by firm break of 55 D EMA (now at 168.56) will delay this bullish case.