Can NuScale’s Soaring Share Price Be Justified After Recent SMR Project Rumors?

If you have your eye on NuScale Power, you are certainly not alone. Investors have been buzzing about this stock, and it is not hard to see why. The last year has seen NuScale Power’s share price rocket by 236.2%, and the momentum has only built from there with a remarkable 158.6% year-to-date surge. Even over just the past seven days, the stock has jumped 16.8%. This pattern hints at a powerful shift in how the market views NuScale’s prospects, perhaps driven by newfound optimism about small modular nuclear reactors or broader shifts in the clean energy sector.

That being said, when share prices climb this quickly, investors naturally wonder: are we looking at an undervalued opportunity, or is the stock getting ahead of itself? According to our quantitative valuation screening, NuScale Power earns a value score of 1 out of a possible 6. In other words, it checks off just one box for being undervalued on standard metrics, which is something worth keeping in mind as excitement grows.

Before making any decisions, it pays to pause and look past the headline figures. Up next, we will break down exactly how NuScale fares under different valuation yardsticks, and later, I will share an approach to valuation that provides a deeper, more nuanced perspective than the checklists most investors rely on.

NuScale Power scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

The Discounted Cash Flow (DCF) model helps investors estimate a company’s value by projecting its future cash flows and discounting them back to present value. In essence, DCF considers what NuScale Power’s future cash earnings would be worth if received today, helping to determine whether its stock is undervalued or overvalued.

For NuScale Power, the most recent Free Cash Flow (FCF) stands at -$96.86 million, reflecting ongoing investments and negative cash generation. Analysts provide projections for the next five years, indicating continued negative free cash flow through 2028. The company is expected to turn positive in 2029, with estimated FCF of $15.25 million. The 10-year FCF outlook, based on further extrapolation, forecasts a steady climb, reaching $50.16 million by 2035.

Despite these anticipated improvements, the DCF model values NuScale Power shares at just $1.18 per share. With the current share price significantly higher, this implies the stock is estimated to be 3782.9% overvalued according to this approach.

The Price-to-Book (PB) ratio is a common valuation metric, especially for companies where earnings may not yet be positive or are highly volatile. PB is particularly useful when analyzing businesses like NuScale Power, which are investing heavily in growth and not currently generating substantial profits. For companies with consistent assets on their balance sheet, PB provides a sense of how much investors are willing to pay for each dollar of net assets.

Growth prospects and risk levels play a major role in determining what qualifies as a “fair” PB ratio. Companies expected to grow rapidly or those with lower risk profiles tend to justify higher PB multiples. Conversely, firms with uncertain futures or slower growth may command a lower PB ratio. It is therefore important to interpret PB in the context of industry peers and overall market sentiment.

As of now, NuScale Power trades at a PB ratio of 8.85x. In comparison, the average PB ratio across the Electrical industry is 2.90x, and NuScale’s peers average 22.56x. While simple benchmarking provides context, Simply Wall St’s proprietary “Fair Ratio” approach goes deeper. It calculates a custom PB multiple that reflects not just industry trends, but also the company’s unique characteristics including forecasted growth, profitability, risks, and market capitalization.

This tailored Fair Ratio can better reflect a company’s specific situation than broad peer or industry comparisons. For NuScale, the lack of a calculated Fair Ratio at this time means we cannot definitively judge its valuation purely on this basis. However, comparing its current PB and seeing that it is substantially above the industry average but below its peers suggests that while the market is assigning a growth premium, it may not be extreme. Still, without a Fair Ratio, caution is warranted in drawing strong valuation conclusions from the PB metric alone.

Earlier we mentioned a more insightful way to look at valuation, so let’s introduce Narratives, a powerful and flexible method that helps you truly understand what drives a stock’s fair value. A Narrative is your story about a company, linking the real-world events you believe in with assumptions about future revenue, profit margins, and ultimately what the company should be worth.

Instead of just relying on simple ratios, Narratives connect your outlook on NuScale Power’s business (such as rapid commercialization of SMR technology, partnerships, and growth prospects) with a tailored financial forecast. This approach culminates in a fair value that reflects your unique perspective. You do not need advanced financial skills to use Narratives; this tool is accessible to anyone via the Community page on Simply Wall St, where millions of investors debate and update their views.

Comparing your Narrative’s fair value to today’s price helps clarify whether now is the right time to buy or sell. Narratives also dynamically adjust to news, earnings, and new information, allowing your investment view to stay up to date.

For example, some NuScale Power Narratives forecast a bullish price target as high as $41.69 by baking in surging demand and landmark projects, while the most conservative see the fair value closer to $17 if execution risks remain high.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The US Dollar is undergoing its most punishing run in over two decades — a retreat of roughly 12–13% year-to-date that has seen the dollar index slip beneath the 100 mark and prompted fresh debate about whether a long-running dollar “supercycle” has turned. Markets have rapidly repriced Federal Reserve policy, global growth differentials and safe-haven

OpenAI CEO Sam Altman speaks at the Snowflake Summit in San Francisco in June 2025. He is one of many tech leaders recently to caution that the AI market may currently be overvalued. Justin Sullivan/Getty Images hide caption toggle caption Justin Sullivan/Getty Images Is the AI boom an AI bubble? Wall Street and Silicon Valley

Western Alliance Bank signage is displayed on the company’s Headquarters in downtown Phoenix, Arizona, on April 27, 2023. Patrick T. Fallon | AFP | Getty Images When you can’t repay a bank loan, that’s distressing — but probably not for the bank. But when tens of thousands of people, who had good credit ratings, can’t,

Not for the first time, there is speculation the company might be bought out. The stock of software development, security, and operations company GitLab (GTLB 11.35%) saw a sudden blast of investor interest Thursday. Thanks to the resulting share price spike as the market barreled to a close the day, the tech company’s share price

PU Prime, a global multi-licensed online brokerage, was honoured to be one of the Global Sponsors at the Dubai Forex Expo 2025. Held on 6–7 October at the Dubai World Trade Centre, the event attracted more than 30,000 financial professionals from around the world, marking another milestone in PU Prime’s commitment to industry excellence. Expert

This rare-earth stock is coming back to earth after a rapid rise. But why? The past couple of days have proven to be a rocky road for USA Rare Earth (USAR -15.26%) investors. While the rare-earth stock skyrocketed almost 90% higher from the end of September through the end of last week, investors have relented

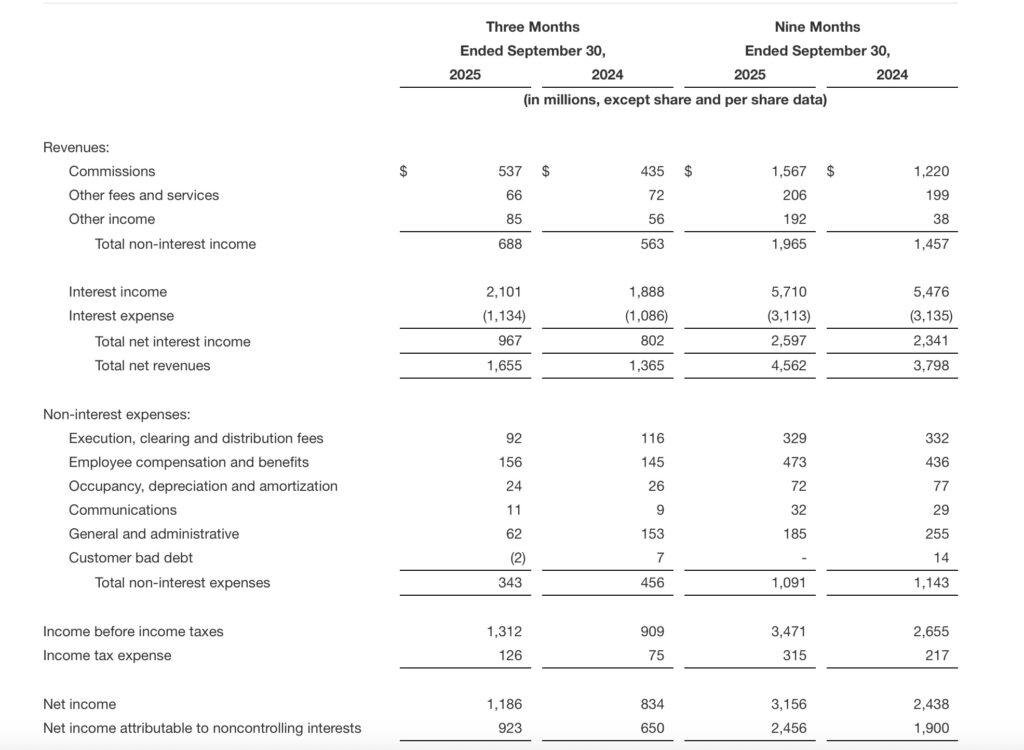

Electronic trading major Interactive Brokers Group, Inc. (NASDAQ:IBKR) today reported its financial results for the third quarter of 2025. Reported diluted earnings per share were $0.59 for the current quarter and $0.57 as adjusted. For the year-ago quarter, reported diluted earnings per share were $0.42 and $0.40 as adjusted. Reported net revenues were $1,655 million

By Noel Randewich Wall Street fell on Thursday, with signs of weakness in regional banks spooking investors already on edge over China-U.S. trade tensions. Regional bank Zions Bancorporation ZION dropped 13% after disclosing an unexpected loss on two loans in its California division, adding to growing investor unease about hidden credit stress as lenders navigate