Quick overview

- The Reserve Bank of New Zealand lowered interest rates by 0.25% amid a cooling labor market and easing inflation.

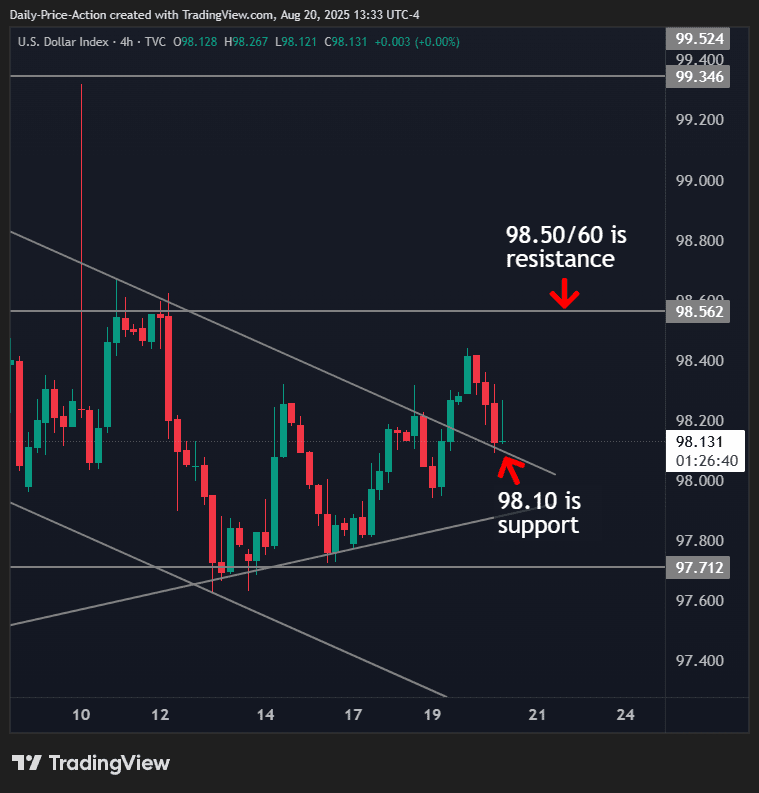

- The U.S. dollar strengthened against most major currencies, driven by resilient domestic data and safe-haven demand.

- U.S. housing starts exceeded forecasts, raising questions about the Federal Reserve’s future rate decisions.

- Geopolitical tensions are increasing, with President Trump noting European nations’ willingness to consider military involvement in Ukraine.

Early today the RBNZ lowered interest rates by 0.25% while later we have Q2 earnings from Target and Analog Devices ADI.

The U.S. dollar closed broadly stronger yesterday, supported by resilient domestic data and safe-haven demand, while global currencies and equities showed mixed reactions to central bank moves and geopolitical risks.

Currency Market Recap

The dollar finished the session higher against most major peers, with the Japanese yen the only exception, edging slightly stronger. The New Zealand dollar weakened sharply ahead of the Reserve Bank of New Zealand’s expected rate cut, while the Canadian dollar slipped following softer inflation figures.

Canada’s July CPI rose 0.3% MoM, in line with expectations, but the YoY rate slowed to 1.7% (vs. 1.8% expected and 1.9% prior). Core inflation metrics also softened:

- Median: 3.1%

- Trim: 3.0%

- Common: 2.6%

Fuel prices dropped 16.1% YoY, housing costs rose 3.0% (driven by rent at +5.1%), while grocery inflation accelerated to +3.4%, reflecting higher fruit, coffee, and confectionary prices.

U.S. Economic Data and Fed Implications

In the U.S., housing starts beat forecasts, climbing to 1.428 million (vs. 1.290m expected), while building permits came in softer at 1.354m (vs. 1.386m expected).

This resilience highlights a housing market that continues to defy higher rates, raising questions about the Federal Reserve’s path. If rate cuts arrive too quickly, the Fed risks fueling inflationary pressures and strengthening economic momentum just as policymakers attempt to balance cooling growth with stable prices.

Geopolitical Landscape

President Trump highlighted growing European urgency to end the Russia-Ukraine conflict, noting that Germany, France, and the UK have signaled willingness to consider stationing troops in Ukraine. He stressed that the U.S. is facilitating potential talks between Putin and Zelensky, while reaffirming Washington’s stance against deploying U.S. soldiers and opposing Ukraine’s entry into NATO.

For markets, rising geopolitical uncertainty could boost safe-haven flows into gold, the dollar, Swiss franc, and yen, while simultaneously weighing on European assets.

Equity Market Performance

U.S. equities ended mixed, with tech and growth sectors bearing the brunt of losses:

- Dow Jones Industrial Average: +0.02%

- S&P 500: -0.59%

- NASDAQ Composite: -1.46%

- Russell 2000: -0.78%

Tech weakness and cautious positioning ahead of central bank meetings dragged on sentiment, while defensive assets found renewed support.

Key Market Events for Today

RBNZ Outlook

A Reuters poll showed 28 out of 30 economists expect the Reserve Bank of New Zealand to lower its official cash rate by 25 basis points to 3.0% today. The cut comes amid a cooling labor market, with unemployment rising to 5.2%, the highest since 2020, and inflation easing to 2.7% in the June quarter, comfortably within the RBNZ’s 1–3% target.

With projections pointing to further moderation toward 2.75% by early 2026, analysts see this move as part of the final stage of the easing cycle. Markets have already priced in the decision, leaving investors focused on the tone of forward guidance, particularly regarding trade tariffs, inflation risks, and employment trends.

FOMC Meeting Minutes

Attention now shifts to U.S. monetary policy. The Federal Reserve will release minutes from its July meeting tomorrow, with two members of the FOMC reportedly voting for an immediate rate cut. On Friday, Fed Chair Jerome Powell will deliver remarks at the Jackson Hole Summit, where investors hope to gain clearer direction on the Fed’s policy trajectory for the remainder of 2025.

Two major companies are set to report before market open (BMO), with analysts closely watching sector trends and guidance.

Analog Devices (ADI) – Q3 2025

- Report Time: Before Market Open

- Expected EPS: $1.95

- Focus: Semiconductor demand outlook, AI-driven growth, and supply chain commentary.

Target Corporation (TGT) – Q2 2025

- Report Time: Before Market Open

- Expected EPS: $2.18

- Focus: Consumer spending patterns, inventory levels, and margin resilience.

Last week, markets were quite volatile once, with gold retreating and then bouncing to finish the week close to $4,000 but yesterday it retreated again. EUR/USD continued the upward move toward 1.17, while main indices closed higher. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

Gold Holds Key Support

Gold prices briefly dipped below $3,268/oz following the Federal Reserve’s decision last week to keep rates unchanged. After recovering, the metal settled at $3,500/oz, still down $21.52 (-0.63%) on the day. Despite the pullback, technical momentum remains tilted to the upside, supported by the 20-week simple moving average and steady U.S. labor market conditions. The $3,450–$3,500/oz zone remains a crucial breakout region for bulls, as investors weigh monetary policy stability against safe-haven demand.

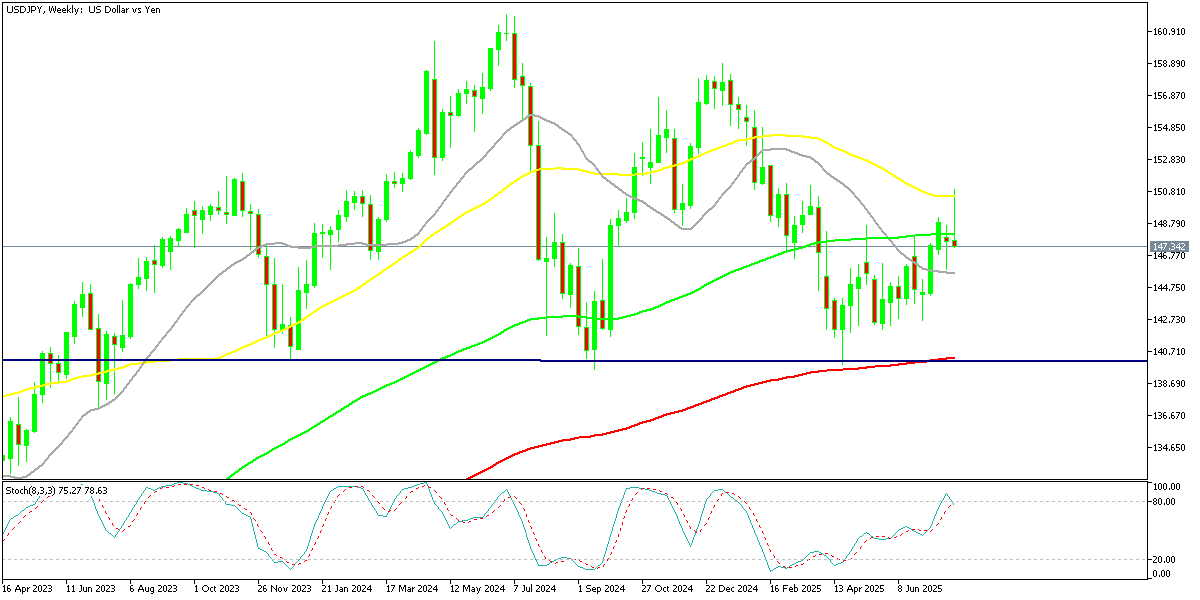

Yen Recovery from ¥150 Shock

In FX trading, the dollar briefly climbed above ¥150 earlier in the week, driven by yield differentials and Japanese capital outflows. However, profit-taking combined with weak U.S. jobs data strengthened the yen, pulling USD/JPY four yen off its highs. The move highlighted ongoing volatility in currency markets, with traders balancing Fed policy expectations against Japan’s efforts to curb yen weakness.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Heading to $112K Support Again

The cryptocurrency market has remained active through the summer. Bitcoin (BTC) surged to record highs above $123,000 in July and $124,000 in August, fueled by institutional demand and technical momentum. Optimism suggested BTC could be approaching the $150,000 mark.

However, enthusiasm faltered after Treasury Secretary Scott Bessent confirmed the U.S. would not expand Bitcoin reserves and inflation data came in hotter than expected. This triggered a sharp correction, dragging BTC down to $113,000 over the weekend.

BTC/USD – Weekly chart

Ethereum Retreats From Resistance

Meanwhile, Ethereum (ETH) has surged past $4,300, its highest since 2021, and appears poised to challenge its all-time high of $4,860. The rally has been driven partly by retail enthusiasm, but fresh institutional flows and bullish chart setups provide additional support.

ETH/USD – Daily Chart

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank’s local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.